The policy rate of the Central Bank of the Republic of Türkiye (CBRT) is the one-week borrowing interest rate for banks. Changes in the policy rate are expected to pass through to loan and deposit pricing. However, this passthrough may be affected by banks’ expectations, liquidity conditions, macroprudential regulations and risk perception. In this blog post, we examine to what extent and how the CBRT’s policy rate cuts made since July 2025 have been reflected in deposit rates and loan rates across different maturities.

For banks, the policy rate is the interest rate at which they can borrow when they need Turkish lira liquidity. If a bank that has access to borrowing at the policy rate sets its deposit pricing at a much higher rate than the policy rate, its funding costs increase. Pricing significantly below the policy rate, on the other hand, may lead to a decline its deposits.[1] Thus, a central bank influences deposit rates through the changes in its policy rate.[2]

Central banks’ policy rate changes may have a different impact on loan rates than they have on deposit rates. In pricing loans, banks add regulatory costs and profit expectations to the costs of funding. Moreover, as loans are of longer term nature than deposits, macroeconomic expectations, those for inflation in particular, and the default risk also play a decisive role in loan rates.

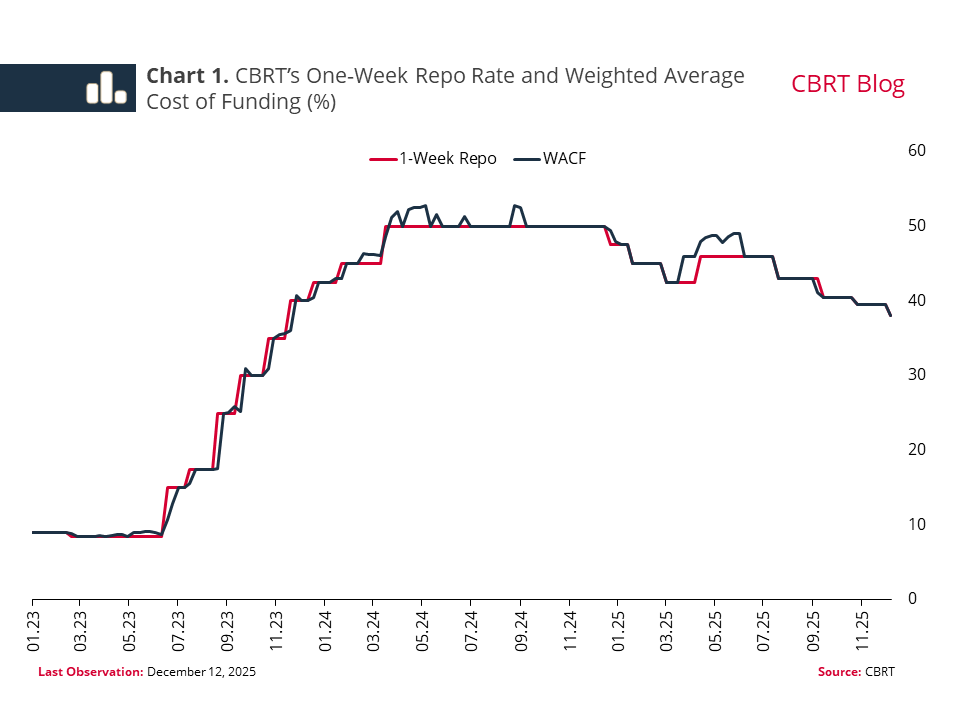

To assess how policy rate decisions translate into costs for banks, we should first look at the cost of liquidity that the CBRT provides to the market. In this respect, the weighted average cost of funding (WACF) serves as an important indicator. Having raised the WACF above the policy rate in March 2025, the CBRT brought it back to the policy rate in June on the back of the improvement in the inflation outlook. Based on the CBRT’s policy rate actions, the WACF has recently been hovering around 38% (Chart 1).

So, do policy rate cuts affect loan and deposit rates? To answer this question, we examined the impact of the policy rate cuts delivered between July and October 2025 on loan and deposit rates. There is an important consideration not to be overlooked when measuring the impact of the policy rate on banks’ pricing behavior: In an environment of predictable policy signaling, banks price in policy rate cuts in advance. In fact, as the June inflation reading released on July 4 came out lower than expectations, the policy rate cut expected on July 24 began to be reflected in loan and deposit rates ahead of the actual decision. Therefore, to better capture the effects, our analysis is based on a period beginning two weeks prior to the start of the rate cut cycle.

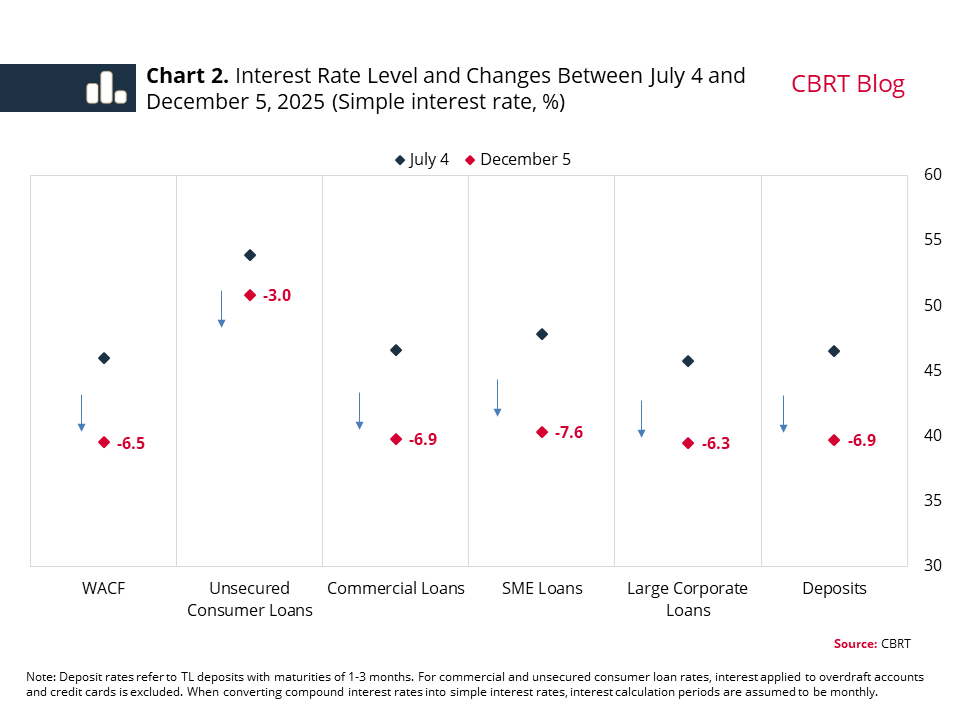

The CBRT cut its policy rate by a total of 650 basis points between July and October 2025. These rate cuts had a significant impact on banks’ interest rates between July 4 and December 5, 2025 (Chart 2). While interest rates on TL deposits and commercial loans decreased by around 690 basis points, those of consumer loans fell by around 300 basis points. An analysis by firm size reveals that loan interest rates declined by 630 basis points for large firms, while a stronger reduction of 750 basis points was observed for SMEs. We believe that the relatively moderate fall in unsecured consumer loan rates was mainly driven by the macroprudential limits imposed on loan growth. These findings suggest that the policy rate cuts were largely reflected in banks’ loan and deposit pricing.

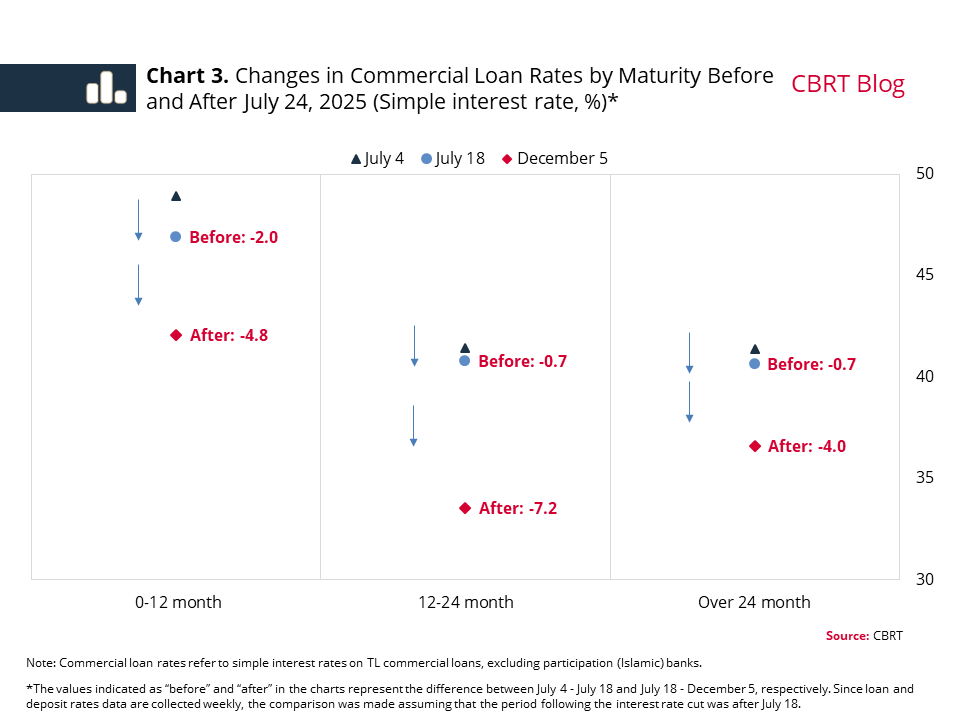

While short-term interest rates are directly affected by changes in the policy rate, long-term interest rates are also shaped by factors such as inflation expectations and the risk premium. Over the study period, the total policy rate cuts of 650 basis points passed onto commercial loan rates as reductions of 480, 720, and 400 basis points for maturities of 0-12, 12-24, and over 24 months, respectively (Chart 3). In this framework, after July 24, long-term interest rates decreased in line with the decline in the country risk premium and the improvement in inflation expectations.

In conclusion, our findings highlight three key points. Firstly, the CBRT’s policy rate cuts are clearly reflected in loan and deposit rates. Secondly, developments in loan and deposit rates suggest that interest rates of short-term loans and deposits are determined by the policy rate, whereas those of long-term loans and deposits are predominantly determined by expectations and risk perceptions. Thirdly, to ensure a sustained decline in long-term interest rates, inflation expectations must be anchored and the risk premium must be contained. Accordingly, maintaining the tight monetary policy stance is critical for affecting loan and deposit rates as well as achieving a sustainable policy rate transmission mechanism.

[1] A similar mechanism is at play when there is excess liquidity in the market, and the deposit rates materialize at levels close to the policy rate.

[2] In practice, deposit pricing below and above the policy rate may also be observed. Factors such as banks’ collateral positions, risk perceptions and appetite for growth also shape deposit rate decisions.